Guest post: Is your business required to offer insurance this year?

This is a guest post from Covered California for Small Business.

Health Insurance Rules Changing In 2016 for Businesses Considered Large; Those With 100 or Fewer Employees Could Still See Big Advantages Through Covered California for Small Business

When it comes to the Patient Protection and Affordable Care Act, many employers have to determine if their business is required to offer health insurance to their employees under the law. This requirement varies based on size, and it broadened its scope in 2016.

Firms with 50 or more “full-time equivalent” (FTE) employees are now considered applicable large employers (ALE) and will need to offer insurance to at least 95 percent of that workforce by this year, up from 70 percent in 2015. Failure to do so could result in a penalty.

Since 2014, small businesses employing between 50-99 FTE were given a waiver from the mandate. But starting in 2016, they too must offer insurance to full-time workers. The good news is that these businesses can now participate in the Small-business Health Options Program, or what in California is called Covered California for Small Business.

California companies with more than 100 employees are not eligible and must purchase insurance on the large group market. For companies with 100 or fewer FTE, Covered California for Small Business can be a huge advantage.

It puts business owners in control of their health insurance budget with a defined contribution, while allowing employees to choose from affordable, name brand health plans from private insurance companies. Companies can also offer their workforce a dental PPO through the program without any minimum participation.

How Covered California for Small Business works is by creating large pools of companies looking to purchase health insurance which then generates the buying power that only large firms have had in the past. Participation carries no administrative fees, no late fees, and billing is consolidated across all health carriers then delivered through a customer first, single-source solution.

Through Covered California for Small Business, employers could also be eligible for a tax credit to offset some of the cost of providing health insurance. Those with 25 or fewer FTE employees and cover half the cost of employee monthly premiums may qualify for federal tax credits, but only if they enroll through Covered California for Small Business.

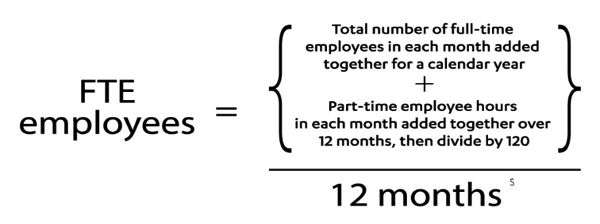

To determine whether an employer is a small or large employer as defined by the Affordable Care Act and applicable California law, the employers are required to calculate their total number of FTE employees.

This number determines whether the employer is eligible to go to Covered California for Small Business to purchase health insurance for its employees. A visit to the IRS website can give you the full details.

Companies that have a common owner or otherwise related generally are combined and treated as a single employer. They must comply with ALE requirements to offer health insurance to their workers even if those companies individually employ fewer than 50 FTEs. The penalty for not complying is determined separately for each related company.

An ALE, including those with 50 to 100 employees is subject to the “employer shared responsibility payment” for not offering insurance to employees.

This penalty is a per-month, per-employee fee for employers who do not offer health coverage to the required amount of full-time employees (as well as their dependents up to age 26).

The regulations, guidance and provisions around the Affordable Care Act are complex and literally span thousands of pages. To help businesses comply, the law includes a number of “safe harbor” provisions.

A safe harbor can reduce an employer’s liability under the law through demonstrating a good-faith effort to comply with its provisions.

For a complete list of eligibility guidelines, visit Covered California for Small Business, or contact a Certified Insurance Agent, www.coveredca.com/forsmallbusiness or call (844) 269-3761.