Small businesses see significant gains from the ACA

The current administration and Congress have made repeated attempts to repeal or undermine the Affordable Care Act. While congressional efforts to fully repeal the law failed in 2017, Congress did significantly alter the ACA by repealing the individual mandate penalty in the December 2017 Tax Cuts and Jobs Act. Since then, the administration has also announced changes that will undermine the individual marketplace by creating separate risk pools, including increasing the length of time a person can use short-term health insurance and allowing associations to offer group plans that don’t meet the ACA’s requirements. These changes ignore the significant benefits the small business and self-employed community has enjoyed from the ACA.

Since its implementation, the ACA has provided health insurance to more than 20 million individuals who otherwise couldn’t access coverage, millions of whom are small business owners, self-employed entrepreneurs or work for small employers. In fact, more than 5.7 million small business employees or self-employed workers are enrolled in the ACA marketplaces, and more than half of all ACA marketplace enrollees are small business owners, self-employed individuals or small business employees. Given recent debate and threats to the future of the ACA, it is critically important for policymakers to understand the law’s benefits to the small business community, which now has access to better, more affordable health coverage.

Prior to the ACA, small businesses and their employees comprised a disproportionate share of the working uninsured. In 2011 more than 6 in 10 of the nation’s uninsured workers were self-employed or working at a company with fewer than 100 employees. However, recent analyses show significant gains in coverage for small business owners, the self-employed and small business employees, with significant decreases in uninsured rates among these populations as a result of both access to ACA marketplaces and the expansion of Medicaid in many states.

Small businesses have also benefited from a stabilization of health care premium increases. Before the ACA was implemented, small businesses paid 18% more on average for health coverage than larger companies, usually for less comprehensive plans. However, after implementation of the ACA, the average annual increase in costs in the small group market dropped significantly, while also making it easier for small business owners or self-employed individuals with pre-existing conditions to afford coverage. Additionally, as this report will show, fears that the ACA would lead to drops in offer rates from employers were unfounded.

While certain provisions of the law need to be strengthened, this report shows that the ACA has been crucial to helping America’s entrepreneurs and their employees access better, more affordable healthcare.

Key Findings

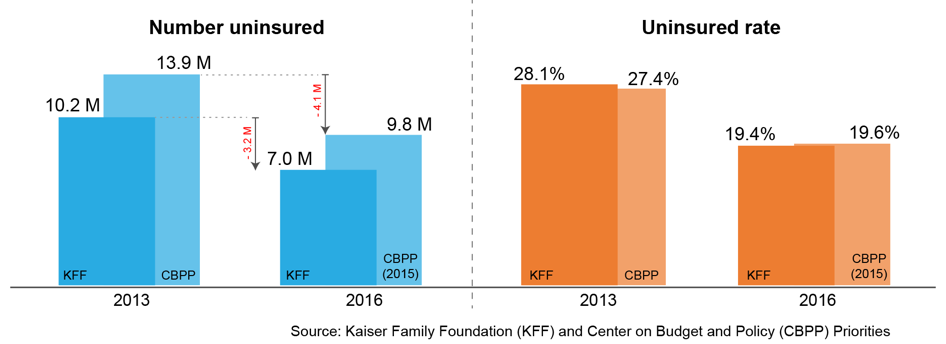

Analysis of small business enrollment after implementation of the ACA found significant decreases in uninsured rates among this group. In 2016, there were 36.1 million people working at a business with fewer than 50 employees. Of those employees, 19.4% were uninsured, down from 28.1% in 2013. Similar research from the Center on Budget and Policy Priorities provides further evidence of significant gains for small business employees under the ACA. According to its analysis, the number of uninsured employees of small businesses (those with fewer than 50 workers) dropped by 4.1 million between 2013 and 2015.

Figure 1: Changes in the uninsured rate for small business employees*

*These findings are based on two different analyses of Census Bureau data.

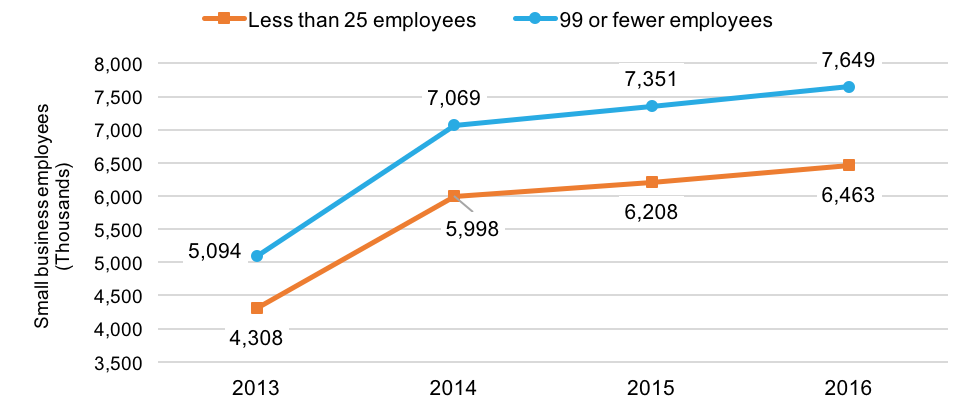

Medicaid expansion has directly benefited small business owners and their employees. An estimated 1.7 million small business employees gained coverage through the expansion of Medicaid by 2015. Overall, there was roughly a 50% increase in the number of small business employees (firms with 99 or fewer employees) enrolled in Medicaid between 2013 and 2016.

Figure 2: Increase in small business employees enrolled in Medicaid

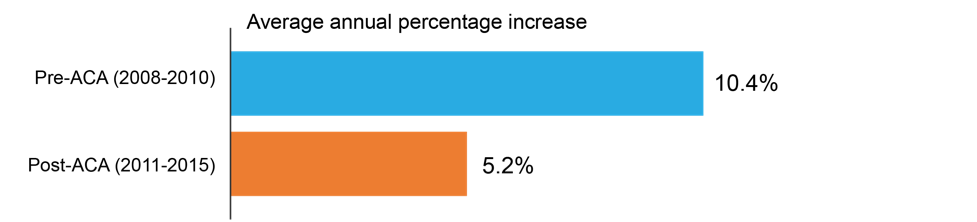

Since 2010, the increase in small business healthcare premiums has been at the lowest level in years, following regular double-digit increases prior to the law’s enactment. In fact, between 2008 and 2010, the average yearly premium increase in the small-group market was 10.4%, according to the Centers for Medicare and Medicaid Services. Between 2011 and 2015, the average increase dropped by half to just 5.2%.

Figure 3: Average yearly premium increase in small-group market dropped by half